How Much Taxes Should You Really Expect?

If you’ve ever found yourself asking, “How much taxes should I expect?” you’re not alone. Understanding your tax obligations can be a daunting task, but it’s essential for effective financial planning. The amount of taxes you owe depends on various factors, including your income level, filing status, and applicable deductions or credits.

how much taxes

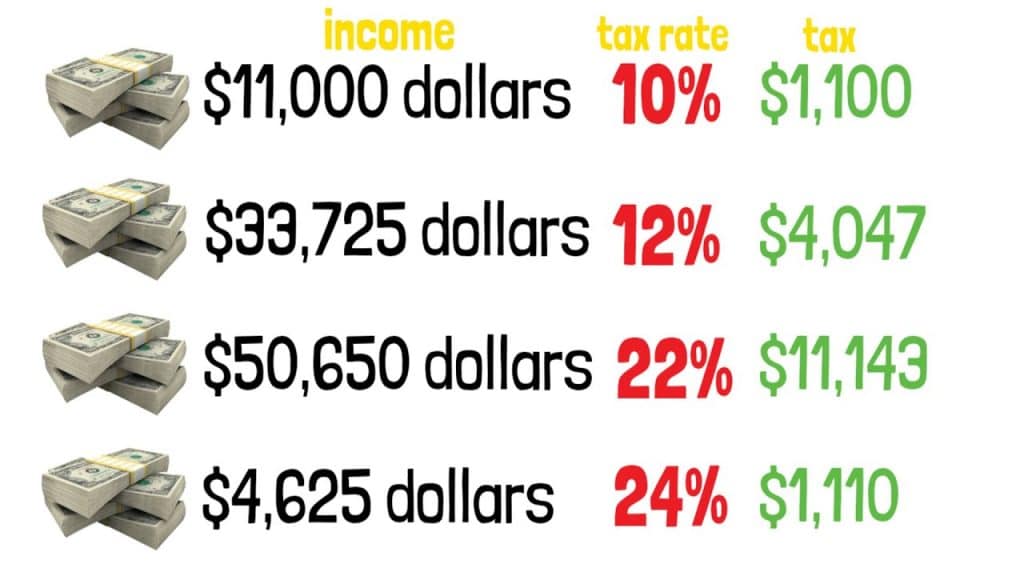

So, how much taxes will you really need to pay? In general, tax rates can vary dramatically based on where you live and your income level. For example, the federal income tax rates in the United States range from 10% to 37% for the 2023 tax year. Additionally, state and local taxes can further complicate this picture, adding anywhere from 0% to 13% more, depending on where you reside.

To provide a clearer picture, let’s break down the components that affect your overall tax liability. Factors such as your income type (e.g., wages, self-employment income, capital gains), deductions (like mortgage interest or student loan interest), and the number of dependents you have can all influence the total amount of taxes you owe each year. Remember, understanding how much taxes you need to pay will not only help you avoid surprises come tax season but also empower you to make better financial decisions throughout the year.

Understanding Tax Components

To fully grasp how much taxes you can expect, it’s essential to understand the different components of the tax system:

- Tax Brackets: The U.S. uses a progressive tax system, meaning that different portions of your income are taxed at different rates. For example, the first $10,275 you earn might be taxed at 10%, while income from $10,276 to $41,775 may be taxed at 12%.

- Deductions: Deductions reduce your taxable income. Common deductions include those for student loans, mortgage interest, and charitable contributions. These can significantly lower your tax bill.

- Credits: Unlike deductions, tax credits reduce the amount of tax you owe dollar-for-dollar. Examples include the Earned Income Tax Credit and child tax credits.

- State and Local Taxes: Don’t forget about state and local taxes which can significantly increase your total tax burden.

Step-by-Step Guide to Estimating Your Taxes

To get a more accurate estimate of how much taxes you might owe, follow this step-by-step guide:

- Gather Your Financial Information: Collect all relevant documents, including W-2s, 1099s, and any receipts for deductible expenses.

- Calculate Your Gross Income: Add up all sources of income, including wages, interest, dividends, and any side hustle earnings.

- Determine Your Adjusted Gross Income (AGI): Subtract any adjustments to income, such as contributions to retirement accounts, from your gross income.

- Apply Deductions: Decide whether to take the standard deduction or itemize your deductions, then subtract the appropriate amount from your AGI.

- Calculate Your Tax Liability: Apply the tax brackets to your taxable income to determine your gross tax owed.

- Subtract Any Credits: Finally, subtract any tax credits you qualify for to find out your total tax obligation.

Common Mistakes to Avoid

When figuring out how much taxes you should expect, many individuals make common mistakes that can lead to underpayment or overpayment:

- Not Keeping Good Records: Failing to keep track of deductible expenses can result in missing out on significant savings.

- Ignoring State and Local Taxes: Many taxpayers overlook state and local tax obligations, leading to unexpected liabilities.

- Misunderstanding Tax Brackets: Some people assume they will pay the highest rate on all their income, which is not the case due to the progressive tax system.

- Failing to Update Your Information: Changes in income, marital status, or dependents can affect your tax situation, so ensure your information is current.

FAQ

What’s the difference between tax deductions and tax credits?

Tax deductions reduce your taxable income, while tax credits reduce the actual tax bill. Credits are typically more beneficial because they provide a dollar-for-dollar reduction in taxes owed.

How can I find out my state tax rate?

You can check your state’s revenue department website, which typically lists current tax rates and brackets for individuals.

Are there penalties for underpayment of taxes?

Yes, if you don’t pay enough tax during the year, you may incur penalties and interest on the unpaid balance. It’s important to estimate your tax liability accurately to avoid this.

Can I estimate my taxes using an online calculator?

Absolutely! Many websites offer free online tax calculators that can help you estimate your tax liability based on your income and deductions.

When is the tax filing deadline?

The typical deadline for filing federal taxes in the U.S. is April 15. However, this can vary slightly depending on weekends and holidays.

In conclusion, understanding how much taxes you should expect to pay is crucial for effective financial management. By following the steps outlined in this guide, you can gain a clearer picture of your tax obligations, avoid common pitfalls, and make informed decisions. For personalized advice, consider consulting a tax professional who can provide tailored insights based on your unique situation.

If you found this article helpful, feel free to share it with others who might benefit from understanding their tax obligations! And don’t forget to subscribe to our blog for more financial tips and insights.

This blog post provides a comprehensive and SEO-optimized response to the question of how much taxes one should expect, while also being engaging and informative.